Oil Above $94 on Iran-Israel Pause and Hormuz Risks — NRG-IA

Geopolitică & Energie Author: Ioana BuzoaicaOil remains elevated after a temporary halt in Iran-Israel strikes, as the market tests the credibility of de-escalation and Strait of Hormuz risks.

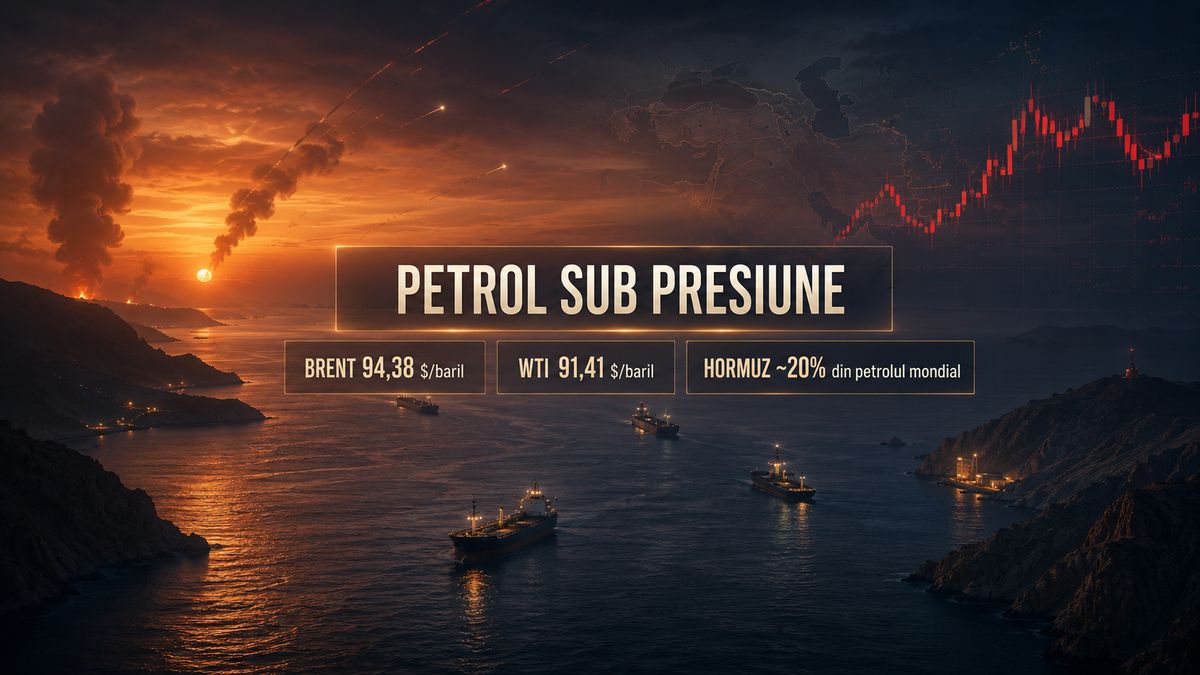

Oil prices remained elevated on Tuesday, June 9, 2026, following a temporary halt in strikes between Iran and Israel. Brent crude edged up 0.14% to around $94.38 per barrel, while West Texas Intermediate rose 0.12% to $91.41 per barrel, according to Reuters. The movement appears modest, but it follows a far more volatile previous session, during which prices surged by up to 5% amid renewed Israeli strikes on Iran and Lebanon. The market subsequently pared some of those gains after Iran announced the conclusion of its wave of military operations against Israel. For the oil market, the stakes no longer lie solely in the actual strikes, but in the credibility of the military pause. Investors are watching whether the de-escalation holds, if political statements are followed by operational calm, and whether Gulf risk remains confined to a risk premium or could translate into supply disruptions. Hormuz remains the market's key vulnerability The Strait of Hormuz remains the primary risk factor for the oil market. A major portion of global oil trade passes through this maritime corridor, and any threat to navigation can quickly feed into Brent and WTI prices. Data from the U.S. Energy Information Administration shows that in the first half of 2025, total oil flows through the Strait of Hormuz averaged approximately 20.9 million barrels per day, equivalent to about 20% of global petroleum liquids consumption. The International Energy Agency also highlights the critical role of the route, accounting for around 20 million barrels per day and roughly a quarter of global maritime oil trade. This share explains the market's reaction. Even without a total disruption of flows, the risk of blockades, vessel attacks, higher insurance costs, or logistical delays can inject a geopolitical premium into prices. In a market already sensitive to inventories, seasonal demand, and OPEC+ policy, the Middle East remains the factor that can rapidly shift price directions. The market tests the gap between military calm and energy risk The temporary halt in strikes eased immediate pressure but did not eliminate uncertainty. Reuters notes that analysts remain skeptical about the durability of the de-escalation, as regional tensions persist and Iran has warned it could resume attacks if Israel continues its operations in Lebanon. This distinction matters for pricing. When the market believes a military pause will hold, oil tends to shed its risk premium. When political signals are ambiguous and regional energy infrastructure remains vulnerable, prices maintain a protective buffer. Brent trading above $94 per barrel shows that the market does not view this episode as closed. At the same time, Tuesday's marginal increase indicates cautious waiting rather than supply panic. Investors appear to be testing every new signal: political statements, military movements, maritime traffic, US reactions, and the behavior of regional producers. The impact quickly reaches fuel prices and inflation For Europe and Romania, expensive oil is transmitted through several channels. The first is the fuel market. Gasoline and diesel react to international price movements, exchange rates, refining margins, taxes, and regional supply dynamics. The second channel is inflation. Oil feeds into the costs of transport, logistics, agriculture, distribution, and industry. A prolonged period with Brent above $90 can sustain pressure on final consumer prices, even if the effect is not immediately visible in every product. The third channel is gas and LNG. Middle East tensions do not only affect oil. If transit risk increases, the market also tracks LNG shipments, shipping costs, and the competition between Asia and Europe for cargoes. While Hormuz has direct relevance for oil, the psychological and logistical impact can ripple more broadly across energy markets. What lies ahead for prices The critical factor in the coming days is whether the pause between Iran and Israel holds. If strikes do not resume and energy transit remains functional, the market may gradually shed its geopolitical premium. If new strikes occur, credible threats to navigation emerge, or signs of blockades in the Persian Gulf appear, prices could react swiftly. For now, Brent remaining above $94 per barrel indicates a market that has not returned to normal. The price reflects not just the barrels available today, but the risk that the world's most sensitive energy route could become harder to secure, traverse, or protect. The headline news is the temporary halt in strikes. The real energy stake is the credibility test of this pause. Oil will react less to diplomatic formulas and more to developments surrounding the infrastructure, vessels, and routes through which energy actually reaches the market.