EIA Forecasts 2003-Low OECD Oil Stocks, Brent at $105 — NRG-IA

Geopolitică & Energie Author: Ioana BuzoaicaEIA projects OECD liquid fuel inventories to fall below 2.3B barrels by year-end, the lowest since 2003, as Brent averages $105/bbl in June-July.

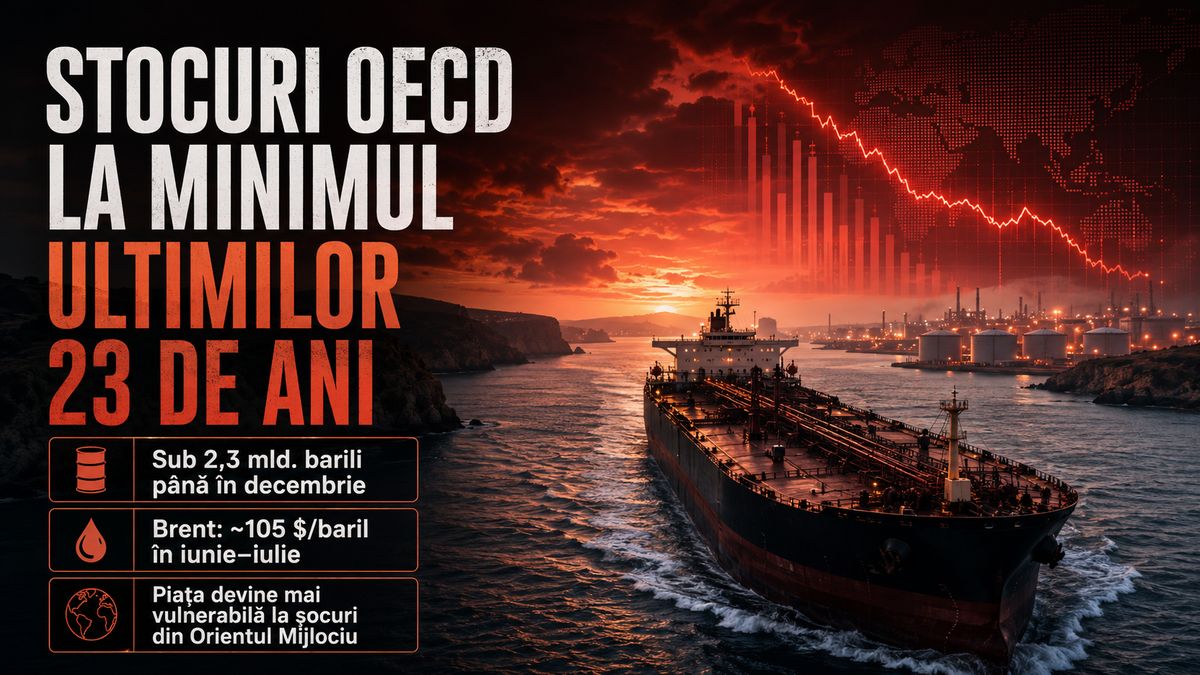

The oil market is entering the summer with an increasingly thin safety buffer. The US Energy Information Administration (EIA) estimates that OECD liquid fuel inventories could fall to just under 2.3 billion barrels by December 2026, the lowest level since 2003, the starting year of the data series used by the institution. The forecast comes at a time when the EIA projects Brent to average approximately $105/barrel in June and July, amid shut-in production in the Middle East, limited maritime flows through the Strait of Hormuz, and accelerated inventory draws to meet global demand. The 2.3 billion barrel figure is the critical benchmark of the report. The five-year average for OECD inventories over the 2021–2025 period is approximately 2.8 billion barrels. The difference indicates a reduction of about 500 million barrels compared to a recent baseline, showing how much the market's operational buffer has compressed. Inventories become the market's central buffer In a normal oil market, inventories absorb demand fluctuations, logistical delays, and localized production outages. In a market strained by a critical maritime corridor, this role becomes far more sensitive. Every barrel drawn from inventories reduces the room for maneuver in the event of a subsequent incident. The EIA estimates average global inventory draws of approximately 6.3 million barrels per day in the second quarter of 2026. This pace reflects the scale of the imbalance between available supply and consumption. The market is operating by drawing down previously accumulated reserves, a mechanism that has physical and commercial limits. Pressure is also visible in the days-of-cover metric. The EIA estimates that OECD inventories could drop to approximately 50 days of demand by the end of 2026, the lowest level since January 2003. When inventories decline in both barrels and days of consumption, the market simultaneously loses volume and reaction time. Hormuz remains the critical variable The Strait of Hormuz continues to concentrate the market's major risk. EIA energy security data shows that total oil flows through Hormuz fell from approximately 20.7 million barrels per day in the fourth quarter of 2025 to 14.6 million barrels per day in the first quarter of 2026. The decline is also significant across components. Crude oil and condensate flows fell from 15.2 million barrels per day to 10.7 million barrels per day, while petroleum product flows decreased from 5.5 million barrels per day to 3.9 million barrels per day. For the global market, Hormuz does not function as a simple regional route. A major portion of Gulf oil exports passes through this chokepoint, and reduced flows force buyers to seek alternatives, draw down inventories, accept higher logistical costs, or temporarily curb consumption. The EIA bases its forecast on the assumption of a gradual reopening of traffic through the Strait of Hormuz and a progressive resumption of trade flows. Even under this scenario, the agency estimates that OECD inventories will continue to decline until the end of the year. Demand falls, but the market remains tight An important element of the forecast is the reduction in global demand. The EIA estimates a 1.1 million barrels per day decline in world oil consumption for 2026, marking the first annual contraction since 2020. This is a sharp revision. In previous forecasts, the EIA still projected demand growth for 2026. The shift reflects the combined effect of high prices, reduced fuel availability, and government measures to curb consumption. While this drop in demand limits price pressure, it does not eliminate tightness in the physical balance. The EIA estimates global liquid fuels production at 99.0 million barrels per day in 2026, down from 106.1 million barrels per day in 2025, while global consumption is projected at 102.9 million barrels per day, compared to 104.0 million barrels per day in 2025. The gap between production and consumption explains the inventory drawdowns. The market is consuming less, but available supply is falling more steeply, leaving inventories to bridge the gap. Brent at $105 and the signal to the market The EIA's Brent forecast of approximately $105/barrel in June and July indicates a market where the risk premium remains high. The price reflects not just today's traded barrel, but also the probability that logistical disruptions, shut-in production, and low inventories will impact supply in the coming months. Reuters noted that the spot market can react quickly to diplomatic signals or reports of a halt in direct attacks between regional actors. Prices may drop temporarily when investors anticipate de-escalation. However, the physical balance adjusts more slowly than exchange-traded prices: inventories are slow to rebuild, shut-in production is restarted in phases, and shipping routes resume flows based on safety, insurance, and commercial decisions. The EIA estimates that following the gradual resumption of traffic…